You’ve probably been hearing a lot about the new tax bill Congress passed at the end of last year. The majority of business owners believe they just received a huge tax cut and that, in the years to come, they will have more liquidity to do with as they please. Unfortunately, many will most likely see a reduction of less than 5% in their tax liability.

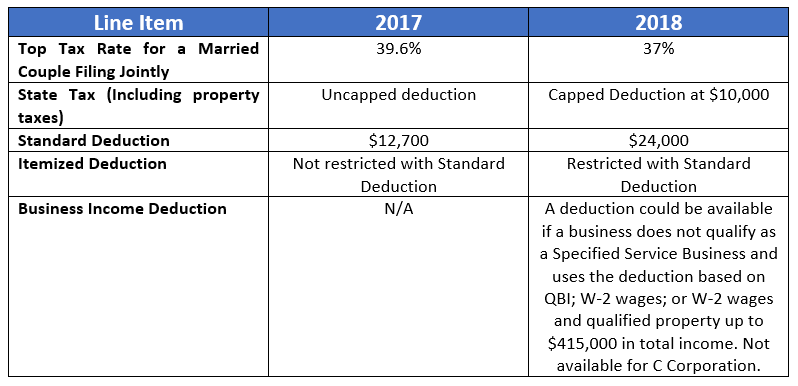

The chart below outlines the specific impact that the “Tax Cuts and Jobs Act” creates for pass-through companies such as S-Corps, LLCs, Sole Proprietorships and Partnerships:

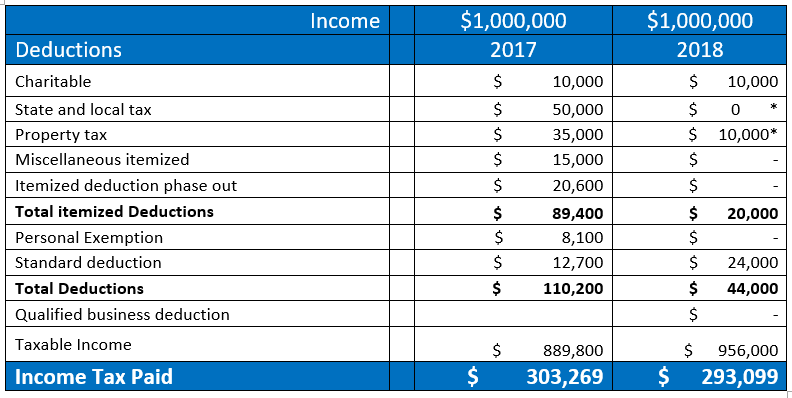

What do these changes mean for pass-through business owners in reality? Below is a scenario showing how the new tax law could affect an S-Corp business owner in 2018:

John and Jane Smith live in a state where they have a 5% state income tax. They also have real estate taxes of $30,000 per year. They do quite a bit of investing and have investment interest and other miscellaneous itemized deductions of $15,000 per year. The Smiths own a Specified Service Business and are not entitled to the new qualified business deduction (QBI) from their Subchapter S Corporation. Between salary, business profits, plus other income, they earn $1,000,000 per year.

Here is how their federal income would be projected in 2017 vs 2018:

As you can see, there is a $10,000 reduction in income taxes owed; however, this is a reduction of only 3.3% in total taxes paid. While any reduction is good, the reduction that the Smiths received is not nearly as great as they (and many other pass-through business owners) may have anticipated.

This is why it is still vitally important for business owners to continue exploring advanced tax planning strategies for their companies. A proactive plan will help ensure that their business is minimizing tax liability without negatively impacting liquidity, creating a greater opportunity to invest resources back into the company and build a more secure future.